Summary Report – Investment Supply Chain Manufacture Of Fabricated Metal Products In Vietnam

01/10/2024

Download report

LATEST REPORT

REPORT OF INDUSTRIAL PARK REAL ESTATE DEVELOPMENT IN VIETNAM

H1-2025

The Global semiconductor market size reached 580B$ in 2022 and is forecasted to reduce slightly in 2023 (557B$) due to the global economic downturn, increasing political conflicts, high inflation, and many countries implementing interest rate hikes, demand has decreased, and there is still a surplus of inventory. With a compound annual growth rate of 6%, in 2030 and 2040, this market is expected to reach 837B$ and 1499B$ thanks to the development of product applications such as: Electronics, Automotive, AI, v.v.

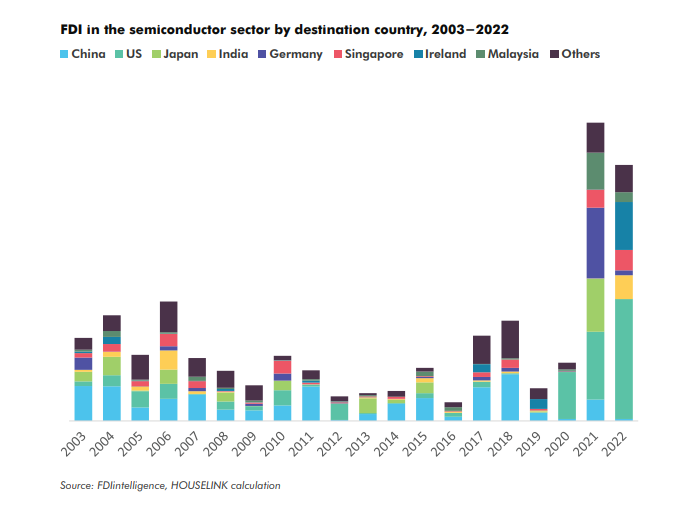

In just two years, 2021 and 2022, the world has witnessed a total Foreign Direct Investment (FDI) capital influx into the semiconductor industry of approximately 155 billion USD. This is the highest FDI inflow level in this industry in the past 20 years. The amount of FDI capital invested in China’s semiconductor industry has significantly decreased (China only accounted for 3% of FDI attraction in the semiconductor industry in 2020). There has been growth in Foreign Direct Investment (FDI) attraction in the United States and in some other countries: Japan, Germany, India, Malaysia, and Ireland.

China, the United States, Germany, France, and Japan are among the largest importers of semiconductors in the world. Meanwhile, Taiwan and South Korea are among the largest exporters. Export and import growth have continued to trend upward since 2019, although the growth rate in 2022 has somewhat declined due to reduced demand for application devices.

In June 2023, Vietnam ranked fourth among Asian countries exporting semiconductors to the United States, following China, Japan and South Korea. Vietnam has the potential to attract investment projects in the semiconductor industry.

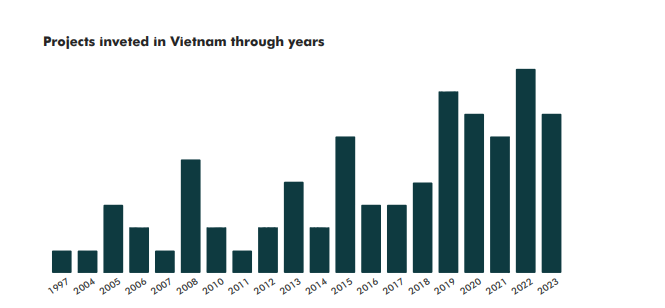

The number of semiconductor industry projects invested in Vietnam is not much, mainly in the field of chip & software design. From 2015 up to now, the project type has been diversified with the entering of other work types, as: simple chip and diode manufacturing, and raw materials projects.

After 2021, the world’s GDP recorded a strong recovery after the Covid epidemic thanks to the promotion of vaccination campagins and the restoration of economic trade. However, in the following year, the global economy suffered a negative impact from the military conflict between Russia and Ukraine, leading to high prices of energy, fuel and inflation.

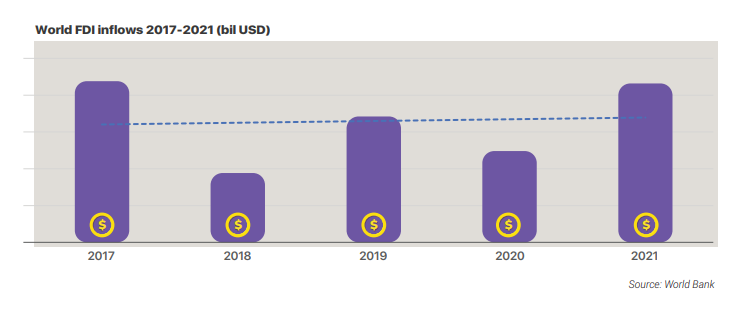

Global FDI was trending slightly upwards from 2017 to 2021. 2020 was heavily impacted by the pandemic in most countries in the world, causing severe economic repercussions. However, in 2022, the application of Covid vaccines has helped us to stabilize to some extent and revive the economy.

Estimated Vietnam's GDP growth for 2022 is expected to increase by 8.02% compared to the same period last year, according to the General Statistics Office (GSO). This is the highest growth rate in a decade. In the context of the world still facing complex economic problems with inflation shocks in many countries at the beginning of 2022 and Vietnam being in the early stages of post-pandemic growth, this growth figure is extremely impressive, demonstrating a very clear economic recovery.

Factors affecting investment in the electricals - electronics industry in Vietnam

Labor factor: Electronics is one of the industries that employs a lot of workers (second only to textile and footwear industries for FDI enterprises), so the labor force is always a pressing issue.

According to Decree No. 31/2021/ND-CP, manufacturing of electronic accessories, components, and electronic modules are among the industries encouraged and enjoying incentives when investing in Vietnam by the Government. In addition, investment projects with a capital of more than VND 6,000 billion (equivalent to about 250 million USD) – large assembly projects investing in Vietnam’s electronics industry according to HOUSELINK’s statistics often have similar capital levels, and also receive investment incentives when investing in Vietnam.

Vietnam industrial real estate infrastructure

We recognize that each region has different location advantages. While the North has many industrial zones near highways, the Central region has the advantage of a long coastline, and industrial zones are also located along coastal roads, making them very close to seaports and convenient for import-export and trade of goods.

Status of investment projects in the electricity and electronics industry

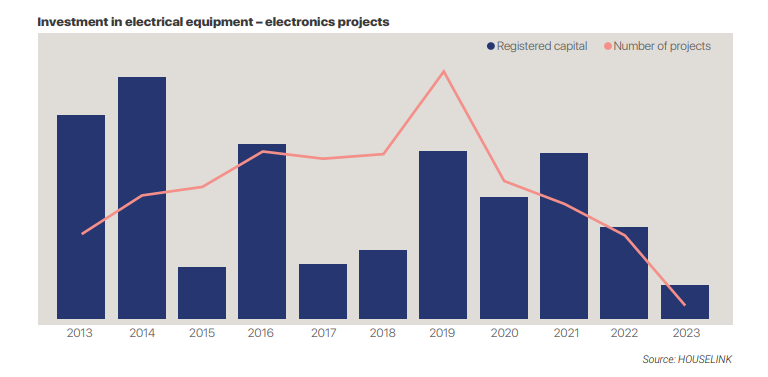

The number of investment projects in the electrical equipment - electronics industry

has shown a continuous increase but decreased during the Covid-19 pandemic

period. So far, there have been no signs of full recovery, but in the first two months of

2023, the scale of capital has shown signs of returning growth.

Looking at the graph describing the situation of attracting investment in the electronics industry since

2013, the number of investment projects into Vietnam has tendency to grow quite steadily in the period

from 2013 to 2019. The average growth rate reached 21.25% in this period, peaking in 2019. However,

when the Covid-19 pandemic began to affect Vietnam (from early 2020) along with the impact from

the global economy-politics, Vietnam recorded a continuous decrease in the number of projects in

three years 2020, 2021, 2022. As of the beginning of 2023, the number of projects has not shown

signs of growth returning.

Northern region excels in attracting investment in the industry

In terms of the number of projects or the scale of registered investment capital, the Northern region still dominates with over 78% of the total number of projects concentrated in the North. Therefore, most large-scale projects choose Northern provinces as investment destinations, with over 81% of investment capital poured into the North affirming the clear direction of dividing investment-attractive industries among the three regions. With such a majority proportion, the Northern region is shaping the trend of investment attraction in the electronics industry for the whole country.

The Year of 2022 is the year that the world economy suffers many negative impacts. The consequences caused by the Covid-19 epidemic, the energy and food crisis caused by the Russian – Ukraine war, which pushed up prices and inflation rate, China is still carrying out the blockade measures to prevent the epidemic, which has made the economy during the 9 months of 2022 very bleak. Facing these economic risks, most of the experts forecasts the economy cannot be recovered in the next quarter, global economic growth still has many challenges in terms of politics, epidemics, and inflation, … In that context, the latest forecast of global GDP growth in 2022 will only fluctuate between 2,4%-3,2%.

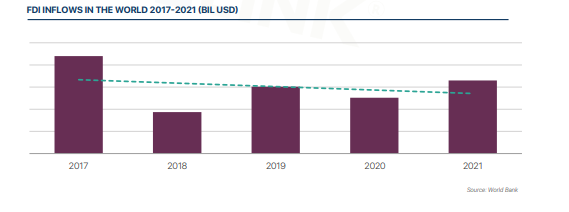

World FDI is on a downward trend from 2017 to 2021. In 2021, global FDI flows increased by 30% compared to 2020. However, in 2022, global FDI is quite gloomy compared to 2021 due to the impact of uncertainly on investor behavior, risks from supply chain disruptions and the increasing of raw material costs and other risks from political and economic conflicts in the world. Global FDI is forecasted to be flat or down compared to 2021.

China is the largest exporter of electrical equipment in 2021 with 898,9 million USD, followed by Hong Kong with 395,5 million USD. In 6 years (2016 – 2021), China has always maintained the leading position in the export market of the electrical equipment industry. Besides, in terms of import market, in the five years of 2016 – 2020, the US is the leading country in the import market of electrical equipment, but by 2021, China has surpassed and become the world’s largest importer of electrical equipment.

Viet Nam’s GDP growth in the third quarter of 2022 is estimated to increase sharply by 13.67% over the same period last year according to the General Statistics Office (GSO). This is the highest Q3 growth rate over the past decade. In the context of complicated world situation with inflation shocks in many countries at the beginning of 2022 and Vietnam is just in the early stages of post-pandemic growth, the growth figure is very impressive, showing that the economy is thriving very clearly.

In the electrical equipment industry, electric wires and cables are among the most exported products. The export value of electric wire and cable products is still showing a clear growth trend. In 9 months of 2022, the export value of this product has a slight increase compared to the same period in 2021. China and the US are two major export markets of Vietnam in this industry.

Status of investment projects in the electrical equipment industry

Investment in the electrical equipment industry showed a continuous increase before 2020 but decreased during the period of the Covid-19 epidemic, so far there is no sign of a full recovery.

In terms of total investment capital, Vietnam’s electronics industry market records 5.5 billion USD in total registered capital and 339 total projects from 2013 to present and heavily depended on the big players in the industry, especially from FDI capital sources. The good news is in 2019 and 2021 recorded many large-scale capital investment projects. The capital flow over the years has fluctuated strongly, not in a clear increasing direction like the number of projects, but in general, there is an increasing trend. Crucially, DDI capital projects in recent years tend to be more flourish, both in 100% DDI capital projects and DDI-FDI capital joint ventures.

The North attracts the largest scale of registered investment capital and the most projects among three regions, especially in the provinces and cities of the Red River Delta economic region.

In term of the scale of registered investment capital, the registered capital in the electrical equipment industry, especially in large scale projects, is mainly located in the Northern provinces over most of the years. Except in 2019, the amount of capital poured mostly into the Southern provinces. Prominent provinces are Bac Giang, Quang Ninh and Ho Chi Minh city. The Central region has a significant project as Vines factory project in Ha Tinh. In which, processing and assembly projects account for the largest amount of capital.

In terms of the number of investment projects,

The North is the region with the highest concentration of electrical equipment projects followed by the South and the projects has scattered distribution in the Central. Since the Covid-19 epidemic appeared, the number of projects has decreased sharply and there is no prospect of recovery in 2022.

Some of the provinces and cities that attract many projects in the electrical equipment industry include Binh Duong, Dong Nai, Bac Ninh, Bac Giang and Long An. We can observe that among the top 5 provinces that attract the most projects, 3 are from the South. This shows that in terms of attracting the number of investment projects, there is not a clear distinction between the North and the South. But in the South, there are a few main provinces, while in the North, investment locations are selected and distributed more widely.

Supply chain of investment in the electrical equipment industry in Vietnam

The investment supply chain has not yet completed, most of the investment projects are processing and assembly type.

From 2013 until now, the supply chain of investment in the electrical equipment industry in Vietnam currently mainly focuses on the processing and assembly type, the components, parts productions ranks the 2nd, the supporting industry segment has not received much attention. In which, the outstanding projects are processing and assembly, account for the large share in our electrical equipment industry both in terms of quantity and registered capital (206 projects and 4,08 billion USD). This is the current situation not only of the electrical equipment industry, but in most industries, investment projects in Vietnam are mainly in the field of processing and assembly. Raw materials are mainly imported from aboard.

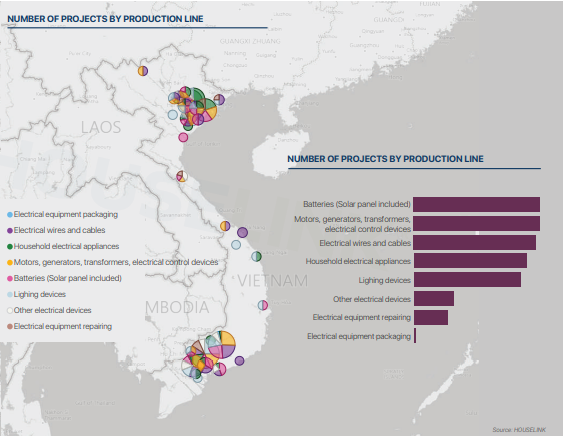

Parts and components production projects are concentrated in the Northern market, the projects here are relatively large. Looking at the map below, currently the Northern market is attracting the most capital sources, where there are projects located in all stages of the industry supply chain, especially the processing- assembly and production of components-parts. In the South, investment capital still mainly comes from processing and assembly projects. We consider that the supply chains in all three regions are incomplete, especially in the support and repair industries.

In the Vietnam market, according to the number of projects, there is an equal attraction among production types. The most prominent is the production of motors, generators, power distribution equipment. The batteries and accumulators’ production are the most attractive type. The second is the production of wires and equipment, followed by the production of electrical appliances and electrical lighting equipment. Most production types have a strong downward trend in 2022. But in terms of growth, battery, and accumulators ‘production projects (especially solar cell production) have grown rapidly, especially in 2021 (increased by 560% in term of total registered capital compared to 2020). Although in 2022, the battery and accumulators’ production projects decrease in the number of projects and registered capital compared to 2021, they are still higher than in other years before. This production type is also considered as one of the most attractive manufacturing industries now.

Electrical equipment projects about to take shape in the future

Based on project data with an investment greater than or equal 2 million USD (equivalent to 48 billion VND) from foreign direct investment (FDI) and domestic direct investment (DDI) sources on the HOUSELINK platform in the field of electrical equipment manufacturing; We synthesize, analyze data, and make reports on projects that are under construction and are in the process of preparation (project preparation, design, contractor selection). All projects have been verified by HOUSELINK.

According to our data, most of the upcoming projects are concentrated in the North (account for 62% of the total project numbers), 23% of the projects are about to be implemented in the South and about 15% of the projects are about to be implemented in the Central region. In the future the North market will continue to be an attractive market for electronics projects. Especially, most of them are projects in the preparation stage, have not yet called for bidding and have not selected a main contractor.

In terms of construction type, in addition to expansion projects of existing investors, Vietnam also attracts a lot of attention from new investors in the electrical equipment industry. Although the number is not too much, the difference between new construction and expansion projects in terms of quantity is not too large, which has partly helped diversify the electrical equipment market in Vietnam in the future.

World socio-economic Overview

After 2021, the world GDP recorded a strongly recover after the Covid-19 pandemic (5,8%) by stepping up the vaccination campaign and restoring economic trade. Still, in 2022, the world economy suffered many negative impacts from the military war between Russia – Ukraine led to fuel prices and inflation raise. Besides, China’s policies of Covid-19 prevention measures, other geopolitical and economic conflicts, and supply chain bottlenecks have reduced the GDP growth forecast in 2022 to 3,2% (according to World Bank).

World FDI is on a downward trend from 2017 to 2021. In 2021, global FDI inflows increase by 30% compared to 2020. However, in 2022, global FDI is predicted quite bleak compared to 2021 because of the uncertainty from investors and risk of supply chain disruptions and raw material costs soaring, and other risks from political and economic conflict in the world. Global FDI this year is forecasted to be flat or lower than the number in 2021.

The electronics industry is one of the fastest growing and strongest industries in the world in recent years. With the diversity of products and services as well as the innovation of production technology, the electronics industry has been and will continue to have a great influence on daily life and activities in the current digital era. According to the Japan Electronics and Information Technology Industries Association (JEITA), the global production value of the electronics and IT industry in 2020 will reach 30.3 trillion USD. In 2021, this value increased by 11% because the Covid-19 pandemic in the other hand is the driving force behind the development of the digital industry (reaching about 33.6 trillion USD). It is forecasted that in 2022, the global production value of the electronics and IT industry will increase slightly by 5% to 35.3 trillion USD.

Viet Nam socio-economic Overview

GDP growth in the second quarter of 2022 is estimated to increase 7.72% over the same period last year, according to the General Statistics Office (GSO). This is the highest second-quarter growth rate in a decade. In the context that the world situation is complicated with inflation shocks in many countries at the beginning of 2022 and Vietnam is just in the early stages of post-pandemic growth, the growth figure is expected to increase. This is extremely impressive, showing that the economy is thriving very clearly. In which, more than 39% contributed to the increase coming from industries and construction sectors.

The index of industrial production (IIP) of the electronic industry has improved significantly since January 2022. The highest number was in March 2022, the IIP index increased quite well to 17.7%. Until August 2022, production at electronic manufacturing enterprises is gradually recovering and developing.

Factors affecting investments in the electronics industry in Viet Nam

Labor Factors

Electronics is one of the labor-intensive industries (only after the textile and footwear industry for FDI enterprises), so the labor force is always an important factor, especially in recent times when there is a serious shortage of high-skill workers in this industry.

Policy factors

According to Decree No. 31/2021/ND-CP, producing electronic components, accessories and assemblies is one of the industries that are encouraged and enjoy incentives when investing by the government. In addition, investment projects with capital greater than 6000 billion VND (equivalent to about 250 million USD) – large assembly projects investing in Vietnam of the electronics industry according to HOUSELINK’s statistics often have similar capital levels, also enjoy investment incentives when investing in Vietnam. Some types of taxes enjoy preferential treatment such as:

The situation of investment projects in the electronics industry

Before the Covid-19 epidemic, the number of electronic projects entering the Vietnamese market grew very well (average increase 19%), peaking in 2019. Since the appearance of the epidemic, the number of projects joined tended to decrease markedly and continuously. After 8 months of 2022, the negative influences from economic and political events in the world have led to investment anxiety, thereby making the number of electronic projects invested in the Vietnamese market is still quite low.

In terms of total investment capital, Vietnam’s electronics industry investment market reaches a volume of 28 billion USD of total registered capital and 1,795 of total projects from 2013 up to now. Besides the investment in this industry heavily depends on the big players in the industry, especially from FDI capital. Typically, the years of 2013,2014,2016 recorded a large amount of capital because big players in the industry such as Samsung and LG entered the market. The good news in 2019, 2020, 2021 was Vietnam market recorded an investment from large electronic technology companies also but the capital trend in other years is downward, apart from a few big players, other investors are still investing in Vietnam with small scale. With this growth rate, in 2022, it is difficult for electronics projects to be recovered.

In recent years, Vietnam has begun to attract electronic projects from many different countries. Korea maintains its leading position in term of investment.

During the period of investing in the electronics industry from 2013 till now, we have recorded several countries in the top countries that invest a lot in the electronics industry in Vietnam such as: Korea, China, Hongkong, Taiwan, Japan. In which, Korea has always maintained the leading position during the past time in terms of both the number of investment projects and the scale of capital.

In terms of registered capital, if in the past, large capital projects mostly came from Korean investors, but in recent years other countries such as Japan, Taiwan, Hongkong, and Singapore have started to choose Vietnam as an ideal location to invest in large-scale projects. In 2022, Korea still leads in terms of investment capital, followed by Hong Kong and Taiwan, but the difference between the countries has been significantly shortened compared to the time before.

According to HOUSELINK’s data, we recorded that in the two years 2021-2022, the Vietnamese electronics market, especially the electronic components industry, has received a number of semiconductor processing and raw semiconductor materials projects, which are favorable signal for attracting more projects in this industry in the future.

Electronics industry investment supply chain in Vietnam

From 2013 till now, the supply chain of investment in the electronics industry in Vietnam is now relatively complete with a full range of investors who have invested in supporting industries, manufacturing-processing of components/accessories/assemblies and the assembling, processing, and finishing of products. Almost projects are mainly and fully located in the North. The number of components/accessories/assemblies projects dominate in our country’s electronics industry but projects of processing, assembling, and finishing of products ranked first in terms of investment capital.

Potential electronics projects in the future

According to HOUSELINK’s data, upcoming projects are mostly concentrated in the North (accounting for 70% of the number of projects about to be deployed). 18% of projects under preparation is in the South and about 12% of projects are located in the Central region. In the future, the Northern market will continue to be a dynamic market for electronics projects. Especially, most of them are projects in the preparation stage, have not yet conducted bidding, and have not selected the main contractor.

Vui lòng hoàn thành biểu mẫu bên dưới để biết thêm thông tin hoặc liên hệ với chúng tôi theo địa chỉ